| Index | Value | 1mo change | 1yr change | 5yr change | Inflation Score |

|---|---|---|---|---|---|

| Economic Inflation | |||||

| Consumer Price Index (CPI) | 237.11 | 0.08% | 1.02% | 7.14% | 2 |

| Producer Price Index (PPI) | 181.50 | -0.55% | -5.02% | -7.30% | 1 |

| 1 Yr Treasury Bill Yield | 0.53% | -0.01 | 0.31 | 0.24 | 2 |

| 10 Yr Treasury Note Yield | 1.83% | -0.07 | -0.25 | -1.58 | 2 |

| Real Interest Rate | -0.49% | 0.35 | -0.73 | 1.33 | 2 |

| US 10 yr TIPS | 0.57% | -0.12 | 0.54 | -0.67 | 2 |

| Capacity utilization | 76.70 | -0.52% | -2.17% | 1.59% | 2 |

| Industrial Production Index | 106.33 | -0.49% | -1.03% | 10.90% | 3 |

| Personal Consumption Expenditure Index | 12,520.04 | 0.58% | 4.18% | 19.53% | 4 |

| Rogers International Commodity Index | 1916.98 | -1.85% | -5.66% | -54.10% | 2 |

| SSA COLA | 0.00% | 0.00% | 3 | ||

| Median Income | $53.657.00 | 0.13% | 7.79% | 3 | |

| Real Median Income | $53,657.00 | -1.48% | -2.31% | 2 | |

| Consumer Interest in Inflation | Stable | 3 | |||

| IAG Inflation Composite | Strong Deflation | 1 | |||

| IAG Online Price Index | Slight Deflation | 2 | |||

| US GDP | 18128.20 | 0.38% | 2.91% | 19.03% | 4 |

| S&P 500 | 1978.35 | 2.01% | -4.89% | 51.66% | 2 |

| Market Cap to GDP | 116.80% | 122.40% | 90.10% | 4 | |

| Corporate Debt as % of Equity | 37.30% | -1.40 | 3.80 | -5.60 | 1 |

| US Population | 323,322 | 0.05% | 0.77% | 4.15% | 2 |

| IAG Economic Inflation Index* | Slight Deflation | 2 | |||

| Housing Inflation | |||||

| Median Home price | 210,800.00 | -1.36% | 4.41% | 35.04% | 4 |

| 30Yr Mortgage Rate | 3.66% | -0.21 | -0.05 | -1.29 | 4 |

| Housing affordability | 171.00 | 5.23% | -6.46% | 4 | |

| US Median Rent | 799.00 | 6.22% | 15.71% | 4 | |

| IAG Housing Inflation Index* | Mild Inflation | 4 | |||

| Monetary Inflation | |||||

| US Govt debt held by Fed (B) | 2,810.10 | 0.29% | 0.60% | 175.10% | 1 |

| US Debt as a % of GDP (B) | 104.26% | 3.76% | 1.28% | 12.18% | 2 |

| M2 Money Stock (B) | 12,485.7 | 0.39% | 5.70% | 41.05% | 4 |

| Monetary Base (B) | 3,891.13 | 2.51% | 1.10% | 74.23% | 3 |

| Outstanding US Gov’t Debt (B) | 18,922,179 | 4.25% | 4.30% | 34.92% | 4 |

| Velocity of Money [M2] | 1.48 | -0.74% | -2.63% | -14.93% | 2 |

| US Trade Balance | -45,677.00 | -5.35% | -4.73% | 3.07% | 1 |

| Big Mac Index | Expensive | 1 | |||

| US Dollar | 98.21 | -1.50% | 2.97% | 27.78% | 1 |

| IAG Monetary Inflation Index* | Mild Deflation | 2 | |||

| Energy | |||||

| Electricity (cents / KW hour) | 12.36 | -2.91% | 1.56% | 3 | |

| Coal (CAPP) | 43.50 | 0.00% | -27.57% | -44.59% | 1 |

| Oil | 33.90 | 0.21% | -31.45% | -65.04% | 1 |

| Natural Gas | 1.71 | -22.76% | -36.57% | -57.85% | 1 |

| Gasoline | 1.32 | 17.92% | -33.23% | -54.37% | 1 |

| IAG Energy Inflation Index* | Strong Deflation | 1 | |||

| Food and Essentials | |||||

| Wheat | 453.25 | -3.00% | -11.73% | -44.69% | 1 |

| Corn | 357.00 | -3.77% | -8.99% | -51.13% | 2 |

| Soybeans | 861.00 | -2.49% | -16.41% | -37.06% | 1 |

| Orange Juice | 127.30 | -3.85% | 5.08% | -27.11% | 4 |

| Sugar | 14.40 | 9.01% | 3.82% | -51.10% | 4 |

| Live Cattle | 136.65 | 0.63% | -10.20% | 20.96% | 1 |

| Cocoa | 2,943.00 | 6.44% | -2.13% | -20.35% | 3 |

| Coffee | 115.65 | -0.13% | -18.15% | -57.47% | 1 |

| Cotton | 56.65 | -6.85% | 12.16% | -71.41% | 1 |

| Stamps | $0.49 | 0.00% | 6.52% | 11.36% | 4 |

| CRB Foodstuffs Index | 333.30 | -1.38% | -6.97% | -32.51% | 2 |

| IAG Food and Essentials Inflation Index* | Mild Deflation | 2 | |||

| Construction and Manufacturing | |||||

| Copper | 2.06 | 0.10% | -23.59% | -54.17% | 1 |

| Lumber | 254.90 | 5.37% | -14.09% | -12.44% | 1 |

| Aluminum | 0.68 | -1.45% | -13.92% | -42.62% | 1 |

| CRB Raw Industrials | 422.60 | 1.17% | -10.38% | -32.42% | 1 |

| Total Construction Spending (M) | 1,140,841.00 | 2.17% | 10.41% | 42.01% | 5 |

| ISM Manufacturing Index | 49.50 | 2.70% | -7.13% | -17.36% | 2 |

| IAG Construction & Manufacturing Index* | Strong Deflation | 1 | |||

| Precious Metals | |||||

| Gold | 1,238.90 | 15.59% | 2.07% | -12.23% | 3 |

| Silver | 14.92 | 4.59% | -10.02% | -56.00% | 1 |

| IAG Precious Metals Inflation Index* | Strong Deflation | 1 | |||

| Innovative Advisory Group Index | |||||

| IAG Inflation Index Composite* | Moderate Deflation | 1 / 2 | |||

* If you would like a description of terms, calculations, or concepts, please visit our Inflation monitor page to get additional supporting information. We will continually add to this page to provide supporting information.

* Our Inflation Score is based on a proprietary algorithm, which is meant to describe the respective category by a simple number. The scores range from 1-5. One (1) being the most deflationary. Five (5) being the most inflationary. These scores are meant to simplify each item and allow someone to quickly scan each item or section to see the degree of which inflation or deflation is present.

* We have also added our own indexes to each category to make it even easier for readers to receive a summary of information.

Inflation Monitor Summary – Composite Ranking

* The Inflation Equilibrium is a quick summary for the whole data series of the inflation monitor. If you don’t like statistics, this is the chart for you.

Inflation Monitor – March 2016 – Introduction

The first quarter of 2016 has been an interesting one. It started off with a significant bout of volatility and risk-off investing. Then after the stock market bottomed in mid-January and re-tested those levels a few weeks later, it has taken off like a rocket. It was almost as if the global economic troubles didn’t exist anymore. Unfortunately, they do… It was almost as if someone (the Fed) waved their magic wand and all the problems of the world just disappeared.

Magic is a beautiful thing. Easter is coming soon. Kids are eagerly awaiting the day where they get chocolate eggs and toys from the magical bunny. What a wonderful thing to believe in magic and illusion.

While many of you don’t believe in the Easter bunny, you probably believe in magic. Earlier this year the markets swooned based on poor economic data, then the Fed told a magical story of how they are data dependent (but only when they want to be) and lowered rate hike expectations and without further consideration the market believed it and started to rise.

Spoiler Alert for those of you who still believe in the Easter bunny, he isn’t real, and neither is this stock market rally.

Sure the prices confirm that stocks and commodity prices have been rising in the past few weeks, but what has really changed? Have US or global economic conditions improved? The only thing that has changed significantly in the past 3 months has been the stock market. So does the Fed’s data dependency include stock prices? Maybe I missed that Fed meeting where they discussed how stock prices determined monetary policy.<end sarcasm>

The Fed’s stated target of four interest rate hikes in 2016 communicated to the public that US economic conditions were strong enough to attempt to return to historically normal rates… At least those were the expectations communicated by the Fed.

At the last Fed meeting, Fed Chairwoman and magician Janet Yellen indicated that the number of rate hikes may be closer to only two. Like magic, the markets rose to greet the new bullish expectations. Apparently, four rate hikes was too much and two was just the right amount. The Fed has a notoriously poor track record of predicting the future of interest rates and inflation. However in this case, there may be another motive.

The Fed has another magic trick in their act other than changing the fed funds rate and printing money. With a few carefully placed words they can change the direction of the stock market. All market participants want to know what the Fed says. They hang on every word uttered by Fed board members. One meeting they predict four rate hikes and the next they reduce it to two. They have not made any actual changes to interest rates, but like magic, they have made everything all right again in the markets.

This is one of the Fed’s greatest tricks, but it is still an illusion. It does not necessarily reflect the global economic conditions. Eventually, market participants will see through the illusion and realize that conditions have not changed and they will have to reassess how that will impact their investments.

Earnings are declining, the global economy is slowing, and commodity prices show this as clear as day – there is a lot less demand than there was 5 years ago. There are a number of reasons behind this enormous drop (upwards of -70%) in many commodity prices. But the biggest one is China. They were consuming 40-60% of many commodities such as concrete, copper, coal, aluminum, steel, and nickel. Their enormous demand to grow drove prices up. Then they withdrew their demand to a large extent, and prices fell. The problem is that this caused misallocation of resources and dislocations of capital. People were assuming that China’s growth would continue. It is hard to say if this growth is stalled or has disappeared completely. Japan went through a similar experience in the 1990s.

This past month, commodity prices have started to rebound a bit, which is causing some people to think the worst is over. Time will tell, but I think it is too early to pop the champagne. Markets generally don’t rebound that quickly and sustain the momentum. It is more likely that this is short covering and end of quarter window dressing. Lets watch how markets react in April.

2016 is a presidential election year… I don’t know why I’m pointing it out other than that I find the whole process amusing. It is like watching a slow motion car wreck or reality TV. You cannot escape the media circus surrounding the potential presidential candidates unless you live in a cave. Even then you might have heard about it. It is hard to miss. Regardless of the comedic value to people like John Oliver, this media circus will have an important influence on markets. For example, Hillary Clinton made some negative comments about drug company reimbursements and immediately afterwards their stock prices dropped. While such statements are probably just pandering for votes, it still affects markets because it may become policy.

Lastly, before you read this month’s charts, what do you think is the best performing commodity this year? Gold! GLD is up 17.42% as of today. You can read more about gold below.

I will leave you with one last question. If a data dependent Fed cannot raise interest rates 0.25% in an economy, which they claim is sound, then how is it possible that the US can ever go back to normal interest rates? Are we going to be stuck with near zero interest rates for the next 20 years? This is not sarcasm, this is a real question that you should ponder.

I hope you enjoy this month’s Inflation Monitor – March 2016.

Kirk Chisholm

As always, please contact me with any questions or to send your feedback. Thank you for reading.

Join our email list to receive the Inflation Monitor sent directly to your inbox.

![]()

Charts of the Month

Global Population Net Migration

Population migration is always happening. People tend to go where they are treated best. Not everyone has the desire to move, but if the conditions are bad enough, they will move. This chart shows where people are moving from and where they are moving to. If you are looking for global markets to invest in, this is a good starting point. The period is from 2008-2012.

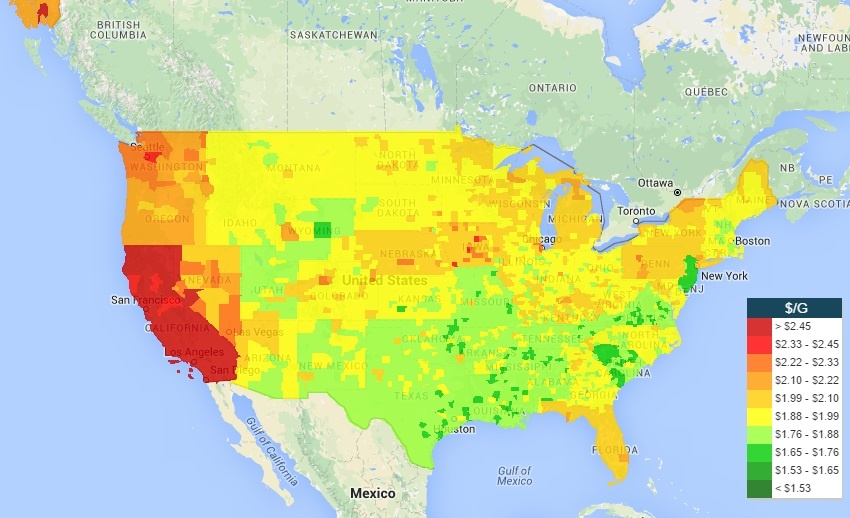

US Median Household Income

This is the US map showing median household income by state.

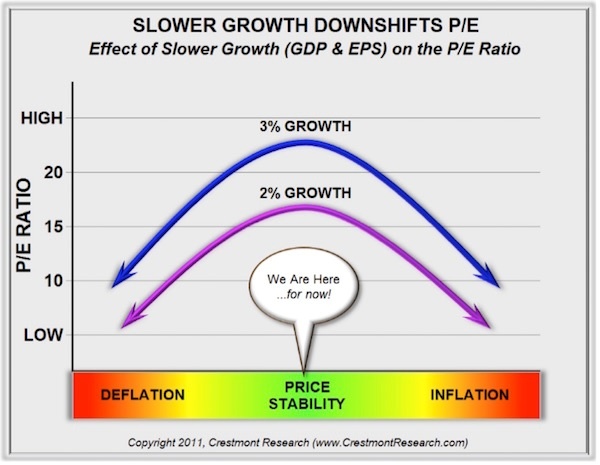

Price Stability

This chart shows the price stability in relation to the rate of inflation. If you want to know where the S&P 500 PE ration should be, it is dependent on the growth rate.

Interesting Inflation Charts

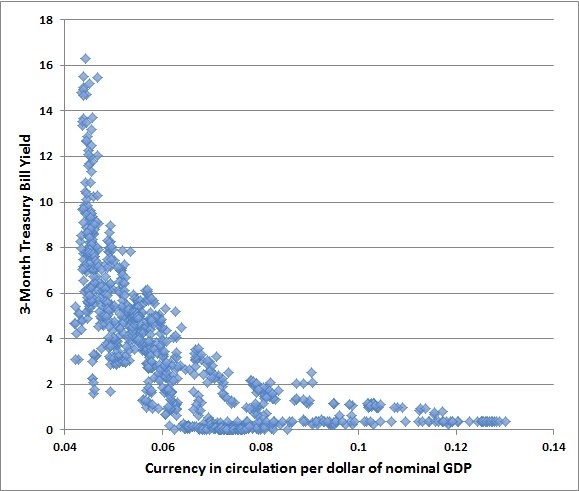

I think I am going to make this chart a permanent part of this inflation monitor so that the importance of it is not missed. John Hussman put this chart in one of his weekly reports a while ago. If I could find the report, I would link to it. You should definitely read his weekly reports. It was a great report about how interest rates relate to the amount of money in circulation. The basic idea is that as rates climb higher, there is less money in circulation, and when rates are low as they are today, there can be an enormous amount of money in circulation without causing high inflation. This idea is a basic concept in economics. However, what is most interesting is seeing this visually.

Think of it this way, if hypothetically the US government can support a debt of $100 at a 5% rate of interest ($5 a year), then how much can the US support at 0.05%? $10,000 or a 100x increase. If rates are at zero, then the number becomes infinite. Now, what if interest rates are negative, why wouldn’t the US print an infinite amount of money?

Obviously, this is hypothetical, but it is important to understand this principal. Once you do, then this is the important part you don’t want to miss. Look at the slope of the curve in this chart. While you may be able to exponentially increase the supply of money without increasing your debt service, the hard part is when you try to increase rates. You will learn very quickly that the debt is unsustainable. If you want to see why interest rates will not rise quickly around the world, this is it. Once you have created $10,000 in debt you will have to reduce it by 99% to reach the 5% rate you had originally. What are the chances of this happening?

Leading Indicators

Dr. Copper

Dr. Copper is still weak, despite the recent bounce. the down trend is still in play. At some point, there will be a tremendous opportunity to buy this essential metal, but right now investors of copper are running for the exits. Much of this has to do with global demand… or the lack of it. For the moment copper seems to be stabilizing… or it could be they are just resting before the next leg down.

Financials

Fed decided to raise interest rates in December. While that should help the financials, trending into negative rate territory around the world may not be the help the Fed initially thought.

Financials have ticked up this month, but the trend in interest rates has not changed. Financials can be a leading indicator, so watch these closely.

Consumer Price Index (CPI)

The CPI is flat for the year. If you have read this Inflation Monitor report for the last 12 months you will know that strong deflationary forces are here to stay. The Fed does not want deflation in the US, but can they stop it? We will find out soon enough what tricks they have up their sleeve.

Producer Price Index (PPI)

The Producer Price Index is continuing to have a rough time this year. The declining PPI might be a reflection of the new economic conditions of producers and manufacturing with a high value of the US Dollar. This makes it harder for US companies to export goods since they will be about 20% more expensive from where they were last year.

US Velocity of Money M2

There is just no sign of stopping this falling safe. I’ll believe in the hyper-inflation tooth fairy when this starts to turn up in a meaningful way.

ISM Manufacturing

There has been a small tick up in the past 2 months. Just under 50, so still not growing, but this index is volatile.

Oil Prices

“We keep thinking that lower energy prices are somehow good for the economy. That can’t be, because energy prices or commodity prices in general don’t drive economic growth. Economic growth drives commodity prices.”

~Stephen Schork

Massachusetts Gas Prices

US Gas Prices

Currency Relative Valuations to Gold

Gold is priced in the currency you use every day. If you live in the European Union, you use Euros, if you live in Japan, you use Yen, and if you live in the US you use US dollars. Each of these currencies are used to buy gold in their respective countries, so we look at gold priced in each country to see how people value it in their own currency. This can tell us a lot about the demand for gold inside and outside the US.

Gold prices are they strong or weak?

The best way to look at any commodity, especially gold, is to compare the commodity to multiple currencies. If gold is rising or falling in US Dollars, that means nothing if the other currencies are not showing the same thing. A true bullish trend in gold is when gold is rising in all (or at least most currencies).

I think it is safe to say from looking at these charts, that gold is currently on a bullish trend in all currencies.

Gold Priced in Euros

Gold Priced in Yen

{kind=link}

Gold Priced in Canadian Dollars

Gold Priced in Australian Dollars

Bonds

TED Spread

A surge in the Ted Spread means a lack of trust in financial institutions. This is not a good trend, although it is off low. It is far off the 2008 highs of 4.6, but the upward trend is not a good sign, since it is confirming many other indicators.

10 year vs. 2 year Treasury Spread

The flattening (or inverting) of the yield curve is not good for banks and also typically shows signs on a recession. It is probably one of the best indicators of a recession we have, yet no one knows the status of whether this indicator still works since interest rates are stuck at zero… sorry 0.25% – 0.50%. What happens if the US has negative interest rates? what will the curve look like then?

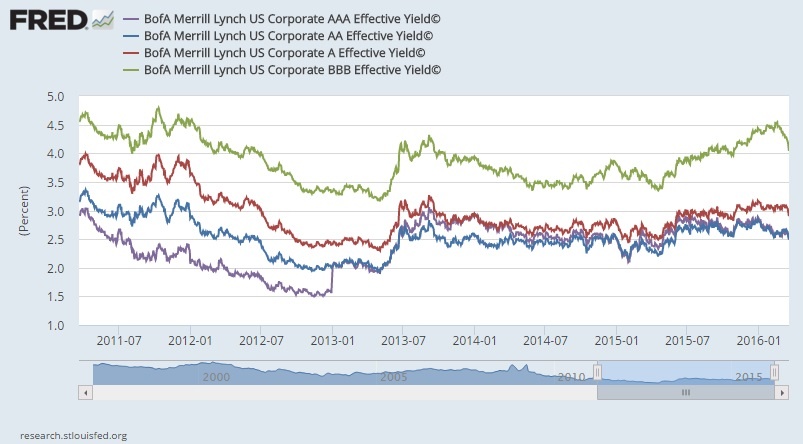

Treasury vs Corp Bond Spread

The spread between 30-year treasuries and corporate bonds is relatively high, as it can be in times of market distress. It will be interesting to see how this plays out as interest rates start to rise… assuming they ever do. Most markets have shown relief from the risk off pressures earlier this year, but this number is still rising.

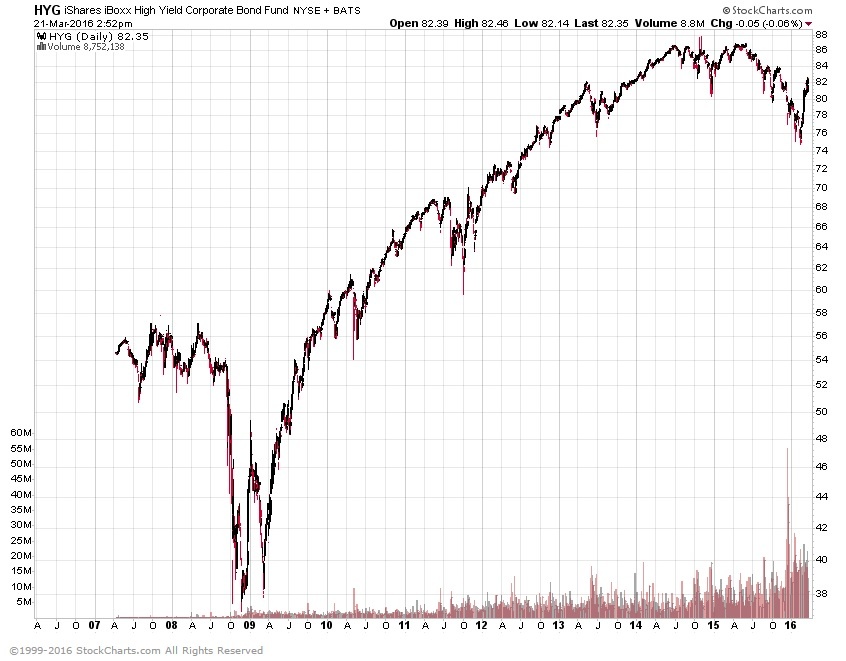

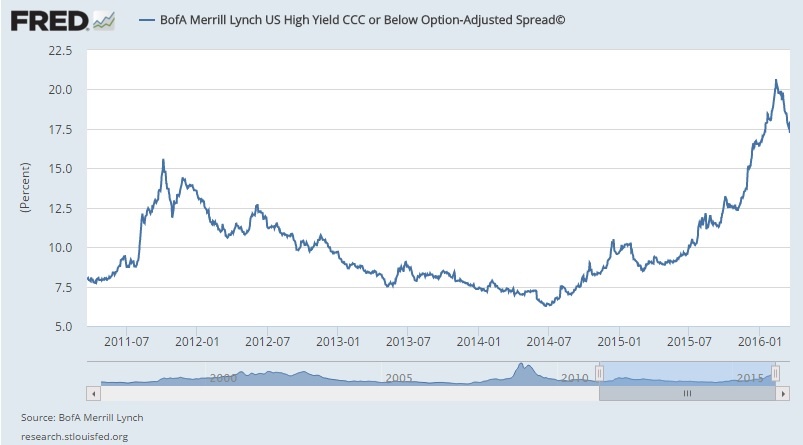

High Yield Bonds (Junk Bonds)

High yield bonds have had a good run of very low default rates. 2014 was around 1%. During recessions, these default rates tend to climb up to around 10% (1991, 2001, 2002, and 2009). This is fine unless you are getting 5% on your high yield bond income. In that case, you would net -5% a year. I’ll bet that is not quite what you had in mind when you were looking for income.

It is important to point out that high-yield bonds are going through a period of turmoil. Recently 3 high yield funds have closed their doors due to investors pulling their money out. You can read about this turmoil and the blueprint for financial contagion in my 2015 year end recap.

This past month high yield bonds have rebounded a bit. Let’s see if this continues.

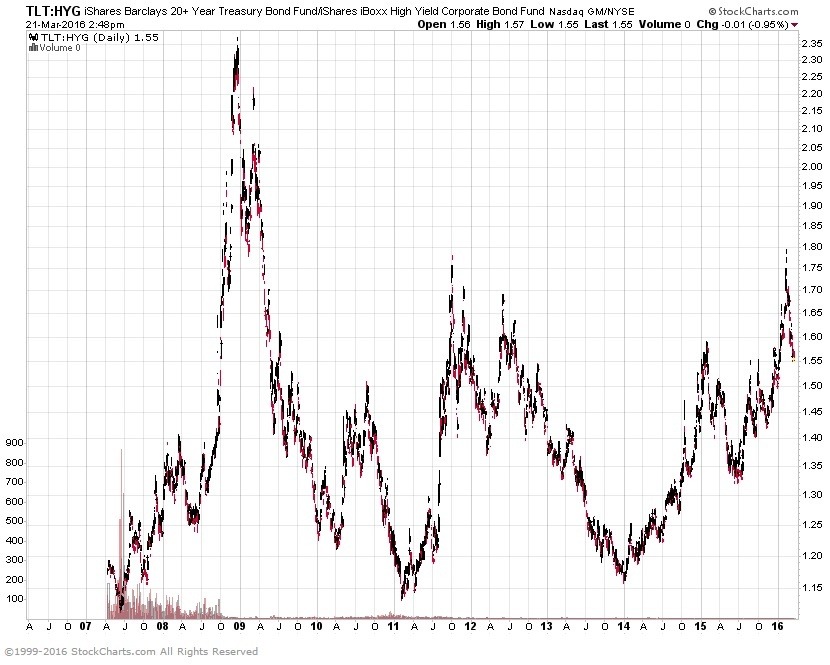

This shows the price of 30-year treasuries vs high yield bonds. The difference has narrowed this past month. While we are now on the higher end of the historical chart, the problems in the high-yield bond market are not fixed so I expect the numbers to stay around these levels or higher.

Bond Yield Spread

High Yield Bond Spread

Some relief in the high yield bond market has appeared. Let’s see if this is a change in trend or a breather in a larger trend.

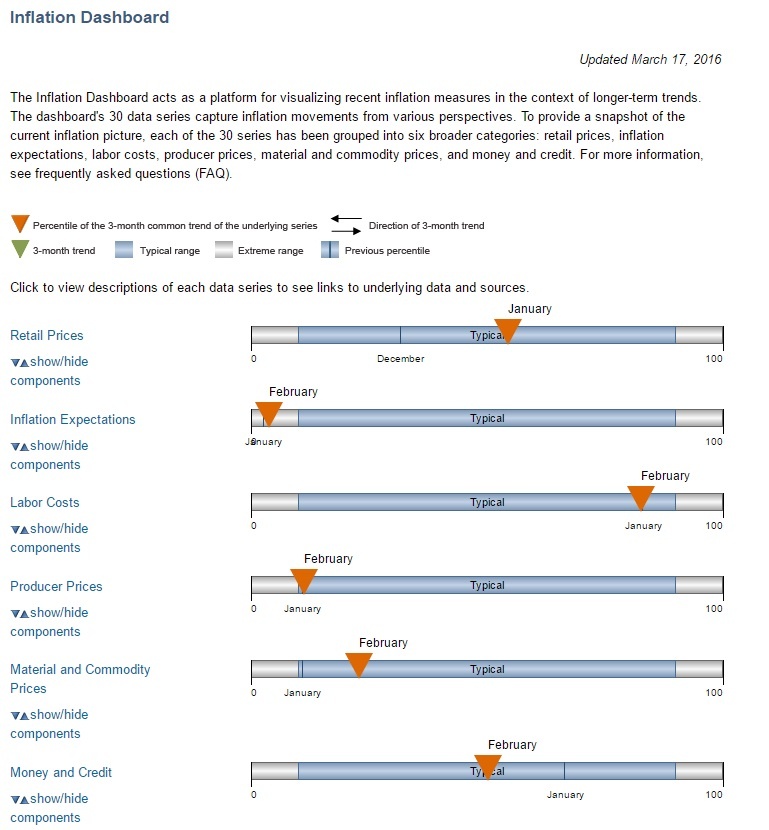

Inflation Dashboard

I like this view from the Federal Reserve because it gives more of a visual perspective of the data presented above.

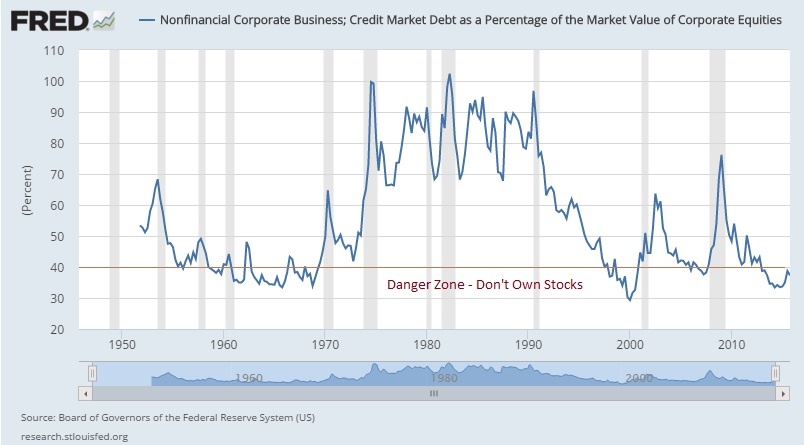

Corporate Debt as a Percentage of Equity

Baltic Dry Index

After breaking below the index all-time lows late last year, it has rebounded a little. It could be the rise in oil prices, or just that the index can only go so low, where any increase in activity would push it up. While this indicator is not all that important, it is just another piece of information that the global economy is not doing well. Until we see a sustained uptick, you should consider the global economy is rough shape.

I hope you enjoyed this month’s Inflation Monitor. See you next month.

Cheers,

![]()

Kirk Chisholm

The IAG Inflation Monitor – Subscription Service

We have been publishing this Inflation Monitor as a free service to anyone who wishes to read it. We do not always expect this to be the case. We expect to charge a small fee for this service starting in 2017. The high amount of interest in this service has put constraints on us to provide more, so this small fee should cover our costs for providing this excellent resource. Our commitment to our wealth management clients is to always provide complimentary access to this research. If you would like to discuss becoming a wealth management client, feel free to contact us.

If you would like to automatically receive the Inflation Monitor in your email inbox each month, click here to join our subscription service.

![]()

Sources:

- Federal Reserve – St. Louis

- U.S. Energy Information Administration

- TD Ameritrade

- National Association of Realtors

- The Economist

- The Commodity Research Bureau

- Gurufocus.com

- Stockcharts.com

- GasBuddy

* IAG index calculations are based on publicly available information.

** IAG Price Composite indexes are based on publicly available information.

About Innovative Advisory Group: Innovative Advisory Group, LLC (IAG), an independent Registered Investment Advisory Firm, is bringing innovation to the wealth management industry by combining both traditional and alternative investments. IAG is unique in that we have an extensive understanding of the regulatory and financial considerations involved with self directed IRAs and other retirement accounts. IAG advises clients on traditional investments, such as stocks, bonds, and mutual funds, as well as advising clients on alternative investments. IAG has a value-oriented approach to investing, which integrates specialized investment experience with extensive resources.

For more information, you can visit: innovativewealth.com

About the author: Kirk Chisholm is a Wealth Manager and Principal at Innovative Advisory Group. His roles at IAG are co-chair of the Investment Committee and Head of the Traditional Investment Risk Management Group. His background and areas of focus are portfolio management and investment analysis in both the traditional and non-traditional investment markets. He received a BA degree in Economics from Trinity College in Hartford, CT.

Disclaimer: This article is intended solely for informational purposes only, and in no manner intended to solicit any product or service. The opinions in this article are exclusively of the author(s) and may or may not reflect all those who are employed, either directly or indirectly or affiliated with Innovative Advisory Group, LLC.