| Index | Value | 1mo change | 1yr change | 5yr change | Inflation Score |

|---|---|---|---|---|---|

| Economic Inflation | |||||

| Consumer Price Index (CPI) | 236.15 | -0.54% | 0.91% | 8.71% | 2 |

| Producer Price Index (PPI) | 201.20 | -1.18% | 0.00% | 13.72% | 2 |

| 1 Yr Treasury Bill Yield | 0.21% | 0.08 | 0.08 | 0.16 | 4 |

| 10 Yr Treasury Note Yield | 2.12% | -0.05 | -0.74 | -1.61 | 4 |

| Real Interest Rate | -0.78% | 0.68 | 0.34 | 0.75 | 4 |

| US 10 yr TIPS | 0.41% | -0.02 | -0.22 | -0.96 | 2 |

| ISM Manufacturing Index | 55.50 | -5.45% | -1.77% | 0.36% | 3 |

| Capacity utilization | 80.10 | 1.01% | 2.04% | 14.92% | 4 |

| Industrial Production Index | 106.66 | 1.26% | 5.21% | 23.11% | 4 |

| Personal Consumption Expenditure Index | 12,143.80 | 0.26% | 4.08% | 22.10% | 4 |

| Rogers International Commodity Index | 2749 | -8.66% | -22.21% | -16.04% | 1 |

| SSA COLA | 0.00% | 1.70% | 3 | ||

| Median Income | $51,939.00 | 1.81% | 3.25% | 3 | |

| Real Median Income | $51,939.00 | 0.35% | -4.56 | 3 | |

| Consumer Interest in Inflation | Mild interest in Deflation | 2 | |||

| IAG Inflation Composite | Mild Deflation | 2 | |||

| IAG Online Price Index | -0.45% | 0.46% | 11.17% | 2 | |

| US GDP | 17599.80 | 1.57% | 4.06% | 22.35% | 4 |

| S&P 500 | 2085.90 | -0.42% | 11.39% | 82.75% | 5 |

| Market Cap to GDP | 121.00% | 125.40% | 115.30% | 80.90% | 5 |

| US Population | 319,485 | 0.06% | 0.70 | 4.00% | 2 |

| IAG Economic Inflation Index* | Stable | 3 | |||

| Housing Inflation | |||||

| Median Home price | 205,300.00 | -1.44% | 5.01% | 20.76% | 4 |

| 30Yr Mortgage Rate | 3.86% | -0.14 | -0.60 | -1.07 | 4 |

| Housing affordability | 165.80 | -0.42% | -1.72% | 2 | |

| US Median Rent | 756.00 | 2.72% | 5.57% | 3 | |

| IAG Housing Inflation Index* | Stable | 3 | |||

| Monetary Inflation | |||||

| US Govt debt held by Fed (B) | 2,705.90 | 3.49% | 39.72% | 312.17% | 1 |

| US Debt as a % of GDP (B) | 101.27% | -0.48% | 2.07% | 18.48% | 2 |

| M2 Money Stock (B) | 11,588.70 | 0.71% | 5.91% | 36.67% | 4 |

| Monetary Base (B) | 3,952.91 | 2.64% | 5.78% | 93.25% | 4 |

| Outstanding US Gov’t Debt (B) | 17,824,071 | 1.09% | 6.49% | 49.66% | 4 |

| Total Credit Market Debt (B) | 57,981.79 | 0.72% | 3.65% | 10.52% | 4 |

| Velocity of Money [M2] | 1.54 | -0.20% | -1.98% | -10.06% | 2 |

| US Trade Balance | -39,001.00 | -7.69% | 8.42% | 4.83% | 4 |

| Big Mac Index | slightly expensive | 2 | |||

| US Dollar | 90.64 | 2.53% | 12.86% | 15.76% | 1 |

| IAG Monetary Inflation Index* | Stable | 3 | |||

| Energy | |||||

| Electricity (cents / KW hour) | 12.58 | -2.78% | 2.19% | 3 | |

| Coal (CAPP) | 55.92 | 5.31% | -13.33% | -2.49% | 1 |

| Oil | 53.71 | -18.61% | -45.58% | -32.32% | 1 |

| Natural Gas | 2.91 | -28.65% | -31.14% | -47.70% | 1 |

| Gasoline | 1.48 | -8.67% | -46.93% | -27.91% | 1 |

| IAG Energy Inflation Index* | mild deflation | 2 | |||

| Food and Essentials | |||||

| Wheat | 590.00 | 1.99% | -2.52% | 8.96% | 2 |

| Corn | 397.25 | 2.06% | -5.75% | -4.16% | 2 |

| Soy | 1023.00 | 0.89% | -20.68% | -1.61% | 1 |

| Orange Juice | 140.25 | -5.94% | 1.01% | 8.38% | 3 |

| Sugar | 14.58 | -6.48% | -11.48% | -45.21% | 1 |

| Pork | 81.08 | -9.64% | -5.31% | 23.59% | 2 |

| Cocoa | 2919.00 | 2.24% | 7.83% | -11.33% | 4 |

| Coffee | 168.30 | -10.22% | 52.17% | 23.84% | 5 |

| Cotton | 60.25 | 0.25% | -28.87% | -20.63% | 1 |

| Stamps | $0.49 | 0.00% | 6.52% | 11.36% | 4 |

| CRB Foodstuffs Index | 369.36 | -5.51% | 0.57% | 7.15% | 3 |

| IAG Food and Essentials Inflation Index* | mild deflation | 2 | |||

| Construction and Manufacturing | |||||

| Copper | 2.83 | -0.65% | -16.86% | -15.55% | 1 |

| Lumber | 331.30 | 0.61% | -7.72% | 41.58% | 2 |

| Aluminum | 0.81 | -9.72% | 1.10% | -20.71% | 3 |

| CRB Raw Industrials | 492.11 | -2.46% | -6.82% | 0.55% | 2 |

| Total Construction Spending (M) | 974,976.00 | -0.28% | 2.36% | 8.12% | 3 |

| IAG Construction & Manufacturing Index* | Mild Deflation | 2 | |||

| Precious Metals | |||||

| Gold | 1,183.20 | 1.49% | -1.79% | 7.94% | 3 |

| Silver | 15.69 | 1.49% | -1.70% | -6.89% | 3 |

| IAG Precious Metals Inflation Index* | Stable | 3 | |||

| Innovative Advisory Group Index | |||||

| IAG Inflation Index Composite* | mild deflation | 2 | |||

* If you would like a description of terms, calculations, or concepts, please visit our Inflation monitor page to get additional supporting information. We will continually add to this page to provide supporting information.

* Our Inflation Score is based on a proprietary algorithm, which is meant to describe the respective category by a simple number. The scores range from 1-5. One (1) being the most deflationary. Five (5) being the most inflationary. These scores are meant to simplify each item and allow someone to quickly scan each item or section to see the degree of which inflation or deflation is present.

* We have also added our own indexes to each category to make it even easier for readers to receive a summary of information.

Inflation Deflation Composite Ranking

* The Inflation Equilibrium is a quick summary for the whole data series of the inflation monitor. If you don’t like statistics, this is the chart for you.

Inflation Monitor January 2015 – Introduction

I hope you had a pleasant holiday season. Now that the eggnog has run out (although probably more likely the rum), your trees and menorahs have been put away until next year, and you are getting back to work in this cold weather (what else is there to do when it is this cold except work). Let’s see what the new year has brought for us as a present. In this month’s issue, I will mainly be discussing oil prices and the US Dollar. The two areas which are generating the most interest.

Deflation still seems to be winning globally, and the US is teetering on the edge of heading into deflation as well. Fortunately, the US economy is growing. Considering what is happening around the world, it might not last more than a few quarters, but for now, the US is a stable island in a sea of deflation.

To start the year I am going to play around with the format a bit to see what works best for people. In this month’s issue, I am planning on breaking the bottom section of the Inflation Monitor into separate excerpts throughout the month based on thoughts or ideas that I have had rather than wait until the end of the month. I will try to spread this out a bit more a see if this is a more desirable setup. While this might be a bit scatterbrained, it might get back to what this section was supposed to be: inflation monitor data, then some ideas, not a lengthy dissertation. This month was difficult to focus on much else since oil has played such a large part of the public’s interest. So we will focus more on oil, interest rates, and the US Dollar.

This is the first issue of the Innovative Advisory Group Inflation Monitor in 2015. We continue to receive a lot of positive feedback on our first few issues of the Inflation Monitor. As you will notice, we have taken some of this feedback and make some minor adjustments to our issues each month. As always, please contact me to send your feedback on how I can make this monthly Inflation Monitor a better tool or resource for you.

Thank you for reading and I hope you enjoy this month’s issue – Inflation Monitor January 2015.

Kirk Chisholm

![]()

Inflation Monitor January 2015 Summary

Why do lower oil prices matter to you?

While gas prices at the pump have been slow to catch up to the drop in oil prices, this will eventually help the consumer. They will have more money to spend in other areas and potentially could spend that money helping the US economy. However, this assumes that people will spend rather than save. I would not make that assumption since consumers have been readily paying down their debts. This also assumes that the drop in oil prices does not reduce the number of jobs needed in the oil and gas service, production and exploration sector. Lower oil prices most likely will reduce jobs.

Here are some ways that the consumer will benefit:

- Lower gas prices at the pump– Nothing more needs to be said about this…

- Lower costs to heat your home- Assuming you use oil or gas.

- Transportation companies: trains, planes and automobiles (a classic comedy), and trucking will benefit from lower oil prices, assuming they have not hedged their prices at a higher level. So your airline ticket prices should start to drop, and other travel related areas.

- Mining companies: whose costs are in large part due to energy prices, should benefit from lower costs.

- Chemical companies: whose product is comprised of petroleum (such as plastic) should also do well.

- Retailers: Some large retailers who transport goods and will also benefit.

Make your Christmas list of stocks to own and be patient.

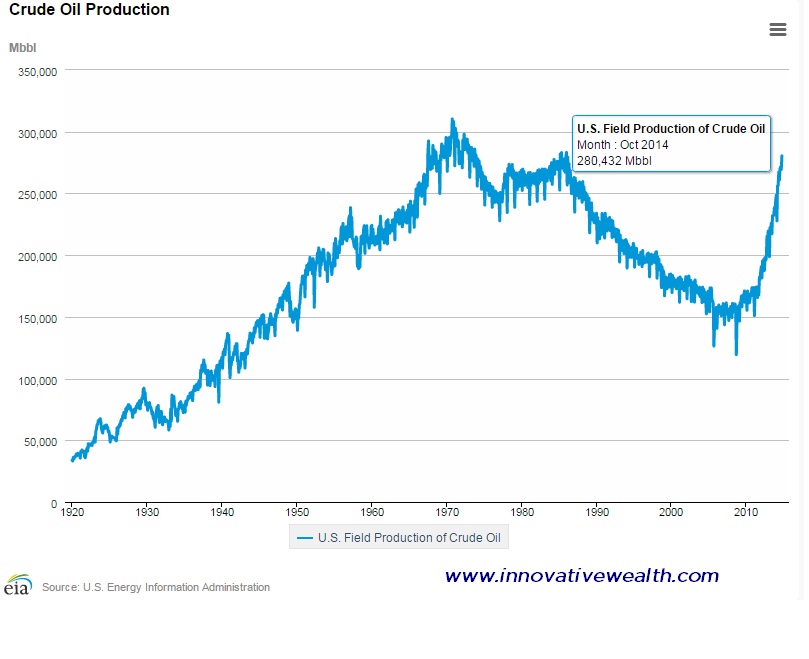

Charts of the Month

US Oil Production

US Oil Prices (WTI)

Gas Prices

All I can say is WTF?!?!

Gas futures are at $1.33 as of when this picture was taken. This past summer they were at $3.15.

Pump prices have gone from $3.29 to $2.59. I guess we know who is going to be flush with cash for a while.

I think I am going to start taking pictures of gas stations around here compared to the futures price of gas so people don’t think this is one isolated example or that I’m crazy. Now it is on the internet. And as we all know, if it is on the internet, it must be true…

US Dollar

You have to go back to 2003 to see the US dollar at these levels. Could we be heading to level not seen since early 2000s?

Interest Rates:

*Research from this picture for the 10 year treasury spread over inflation can be found at Crestmont Research

That is it for this month. I put out 3 supplements for this issue a few days ago, so you can see a continuation of my thoughts about oil here:

- Is it time to buy oil stocks?,

- Where is the price of oil going?,

- What products and uses does Petroleum have outside of Gasoline?

Thanks for reading. I hope you stay warm and enjoy the rest of your winter.

Cheers,

![]()

Kirk Chisholm

![]()

The IAG Inflation Monitor – Subscription Service

We are initially publishing this Inflation Monitor as a free service to anyone who wishes to read it. We do not always expect this to be the case. Due to the high demand for us to publish this service, we plan to offer it free for a while and when we feel we have fine tuned it enough, we do plan on charging for access. Our commitment to our wealth management clients is to always provide complimentary access to our research. If you would like to discuss becoming a wealth management client, feel free to contact us.

Sources:

- Federal Reserve – St. Louis

- U.S. Energy Information Administration

- U.S. Post Office

- National Association of Realtors

- The Economist

- The Commodity Research Bureau

- Gurufocus.com

- stockcharts.com

* IAG index calculations are based on publicly available information.

** IAG Price Composite indexes are based on publicly available information.

About Innovative Advisory Group: Innovative Advisory Group, LLC (IAG), an independent Registered Investment Advisory Firm, is bringing innovation to the wealth management industry by combining both traditional and alternative investments. IAG is unique in that we have an extensive understanding of the regulatory and financial considerations involved with self-directed IRAs and other retirement accounts. IAG advises clients on traditional investments, such as stocks, bonds, and mutual funds, as well as advising clients on alternative investments. IAG has a value-oriented approach to investing, which integrates specialized investment experience with extensive resources.

For more information, you can visit www.innovativewealth.com

About the author: Kirk Chisholm is a Wealth Manager and Principal at Innovative Advisory Group. His roles at IAG are co-chair of the Investment Committee and Head of the Traditional Investment Risk Management Group. His background and areas of focus are portfolio management and investment analysis in both the traditional and non-traditional investment markets. He received a BA degree in Economics from Trinity College in Hartford, CT.

Disclaimer: This article is intended solely for informational purposes only, and in no manner intended to solicit any product or service. The opinions in this article are exclusively of the author(s) and may or may not reflect all those who are employed, either directly or indirectly or affiliated with Innovative Advisory Group, LLC.