“The major fortunes in America have been made in land.”- John D. Rockefeller

After more than 75 years John D. Rockefeller is still considered the richest man in history when you adjust for inflation.

According to the New York Times as of 2007, his net worth reached $192 Billion. Compare this with Bill Gates whose fortune is only $82 Billion. This shows how enormous the fortune of John D Rockefeller actually was. Only Commodore Vanderbilt and John Astor have even come close with $143 Billion and $116 Billion.

Rockefeller at one time controlled 90% of the nation’s oil and his fortune was approximately 1.5% of the nation’s economy. That is legacy wealth. Wealth that is hard to lose of destroy.

Even though all his wealth was made from oil, he still attributes major fortunes being made in land or real estate. That is a powerful statement.

What I am going to discuss here is one of the reasons why real estate is able to create legacy wealth. Wealth that can last for many generations if it is managed properly. Interestingly enough this is also one of the least understood benefits of owning real estate.

This post is the second part of a four part series about real estate. The last post, These Top 7 Powerful Tools Can Create Legacy Wealth from Real Estate, briefly touches on the importance of inflation to your real estate assets. I plan on going into much more depth this week.

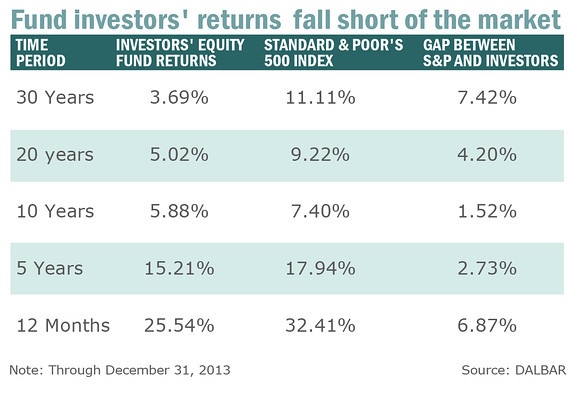

The Advantages of Investing in Real Estate

Real estate is one of my favorite asset classes. Here is why.

In the prior post of this series I touched on a few of the reasons that real estate is such a favorable asset to invest in.

- You can easily use leverage to buy it,

- there is a limited amount of real estate

- Tax benefits

- It can create cash flow

- Appreciation potential

- It is inflation Proof

- You can reduce the debt in real terms over time.

Just one of these alone would be a good enough reason to invest in this asset class, but all 7 make it especially powerful. With exception of the tax benefits and the limited supply of real estate, all of the other benefits rely on inflation to enhance the performance of real estate over time. While I will discuss these in more detail, let’s first discuss what inflation is and how it works.

Read More…